- Blog/

The App layer is a trap

Table of Contents

Satya Nadella said something that most SaaS founders probably don’t want to hear. Business applications, he argued, are at their core just CRUD databases — Create, Read, Update, Delete — with business logic layered on top. In an agentic world, that logic migrates entirely to the AI tier. Agents won’t care about your backend. They’ll update multiple databases simultaneously, orchestrate workflows across systems, and execute decisions. When the logic leaves the app, the product proposition leaves with it.

https://youtu.be/9NtsnzRFJ_o?si=hx5Hl5wtiH5UHVsO&t=2806

The public markets got there first. The SaaS premium, the elevated multiple investors assigned to software businesses on the logic that they scale to near-zero marginal cost has cratered. Companies that commanded 30x, 40x revenue multiples at the 2021 peak have been repriced dramatically. Some have shed 60–70% of their market cap from peak. This isn’t a macro correction. It’s the market pricing in exactly what Satya described.

And it isn’t just happening to enterprise software companies. The same pattern is playing out at every layer of the stack, all the way down to a hobbyist who spent a weekend building an app and found the frontier lab had already shipped their feature as a footnote in a changelog. Different scales. Same wall.

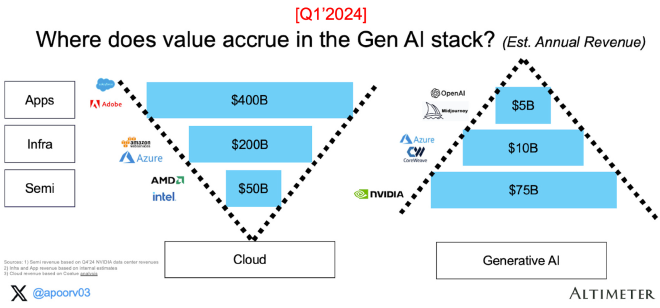

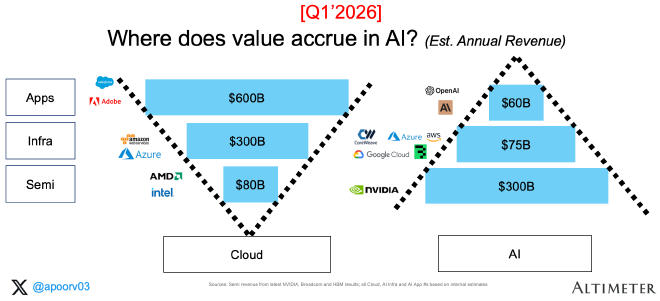

Where does value actually accrue in AI? #

Think about the AI stack in three layers: applications at the top, infrastructure and inference in the middle, semiconductors and frontier models at the base.

I came across an article by Apoorv Agrawal, partner at Altimeter, that I’d genuinely recommend reading in full. It’s one of the clearest pieces I’ve found on where the money actually flows in generative AI, and a lot of what follows draws from his framing. You can find it here.

The cloud comparison is useful but mainly because it shows exactly where AI diverges. Cloud followed classic economies of scale. More customers meant lower unit costs, wider moats, compounding margins. The value triangle flipped upward toward software over time. WS made cloud infrastructure cheap. A generation of software companies built on top and barely touched the hardware. A decade of premium SaaS multiples followed.

AI hasn’t done this. Not yet and there’s a serious argument it won’t, at least not at the app layer.

Apoorv’s data makes this concrete. Over the last two years, roughly $350 billion of new AI revenue was added to the ecosystem. Around 75% of it went to semiconductors. The application layer grew more than 10x in that same period and still barely registered a change in the overall shape of the stack.

The triangle has not flipped. It has become more concentrated at the base. The margin data confirms it. Nvidia’s data centre gross margins are running around 75%. Estimated application-layer margins sit somewhere between 0% and 30%. That gap isn’t a timing lag. It reflects where the structural advantages actually live.

Gavin Baker said something on ‘Invest Like the Best’ that genuinely shifted how I see this. Even accounting for Cursor and Cognition, the most successful AI-native app companies of this cycle, net value at the application layer has been destroyed by AI. The companies seeing the highest value creation share one trait: the highest ratio of utilized GPUs per human. That’s not a software metric. Profits are accruing to energy, data centres, chips, and frontier models. Not to the layer where most founders and product teams are spending their time.

Gavin also made an observation that stuck with me: in venture, the companies that survive are the ones building something not obvious to the world before they could build real scale, something genuinely different, genuinely hard to replicate. A lot of app-layer AI companies fail this test. They’re building obvious things in an era where obvious things get commoditized before they get traction.

Cursor has operated for years as a product company running on Anthropic’s and OpenAI’s models, paying frontier API rates while those same labs marketed directly competing tools to its customers. Claude Code crossed $2.5 billion in annualized revenue and over 300,000 business customers by early 2026. That’s the app layer trap in its most uncomfortable form: your supplier is also your competitor, and they have structurally lower costs than you. Cursor’s response was Composer, their own in-house coding model built on open-source base weights but with 85% of total compute spent on their own reinforcement learning pipeline and post-training stack. Composer 2.5, released this week, matches Claude Opus 4.7 on Cursor’s own benchmark at roughly one-tenth the per-token cost. There is no public API. The model runs inside Cursor only: the IDE, the CLI, the web product. That’s a deliberate choice. Cursor isn’t trying to become a model company. They’re trying to stop being a harness. The move down the stack, owning the model, owning the unit economics, locking the experience inside their own environment, is what fighting the app layer gravity actually looks like in practice.

What this doesn’t mean #

This isn’t an argument that the app layer is dead. It’s an argument about what survival requires. Cursor is real. Sixty-seven percent of Fortune 500 companies are customers.(Link to article). They were processing over a billion lines of code daily in 2025 (Aman Sanger - X). But notice what Cursor is doing to stay there: building proprietary models, internalising inference costs, locking the experience into a closed environment. They’re not resting on distribution. They’re actively moving down the stack.

That’s the distinction worth sitting with. The app layer companies that will survive aren’t the ones who built clean interfaces on top of frontier APIs and called it a product. They’re the ones who accumulated something genuinely hard to replicate: proprietary data, deep workflow lock-in, or like Cursor, the willingness to get into the infrastructure business themselves. Gavin Baker’s framing holds: the question isn’t whether your idea is good. It’s whether it’s different and hard enough that the model companies won’t get there before you’ve built real scale.

Most won’t clear that bar. A few will. Knowing which side you’re on is the whole game.